Tax-Free Retirement

Eliminate Risk, Fees & Taxes

Active Savers & Existing Assets

The Power of Indexing

(Not a commodity. But a strategy!)

There Are Various Ways To Invest Your Money

How Would You Like Your Money To Grow?

5 Core Benefits

Power of Indexing

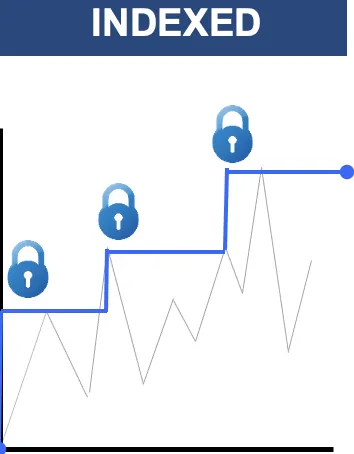

Contributing funds, using a 7702 Plan grow through indexing, an interest-crediting method that enables account owners to have interest credited based on a portion of the rise of a stock market index, while protecting the funds if there is a drop in the index’s value. Through indexing, your savings has the opportunity for growth and, after interest is credited, is protected from losing value when the stock market index drops.

Tax-Free Distributions in Retirement

In addition to the tax-free benefit for beneficiaries, the savings of a 7702 Plan grows tax free and can be accessed tax free as well. You will not usually owe any taxes on funds you access from a properly-structured 7702 Plan through loans, which is the approach being designed.

Access to Funds with No Market-Value Adjustment

Your savings is available to you without adjustment based on the outside market. Because many indexing strategies have a floor of 0% interest credited, when the stock market index is down, your credited savings value will not lose value due to the market. Whenever you need to access your funds, you can do so at full value.

Additional Benefits for the Medical Costs of Aging

Many 7702 Plans include living benefits, which allow an account owner to access a portion of the death benefit while living when certain medical requirements are met. This is to replace your income, if you ever have cancer, stroke, heart attack or you need long-term care. This can be a valuable benefit, as today’s medical expenses in retirement are projected to be hundreds of thousands of dollars.

Inheritance for Your Heirs

This gift from the IRS, provides a benefit for your heirs, above and beyond the value of your account. The benefit is delivered tax-free, so your heirs get the full value of their inheritance.

5 Main Advantages

Use after tax dollars

Grows tax-free

If you need to access money for any reason, you can---there are no strings attached or IRS penalties if you do

Using indexing strategies, your money is protected from market loss—you won’t lose a dime of principle due to market dives

With your contributions, you can deposit larger sums and can make up for years that you didn’t put in the maximum

Powerful Benefits

Reserves - Above FDIC Standard Bank Guarantee

If You’re Not Approved, You Can Get A Surrogate And Still Enjoy The Tax Benefits

Tax-Free Income Does Not Increase Your Social Security Taxes

Principle Balance Protection from Negative Returns via indexing!

Never Pay Taxes On Any of the Gain

Income Does Not Affect FAFSA (Free Application for Federal Student Aid)

No Pre – 59 ½ or 73 Age Rule!

Income Does Not Affect AGI (Adjusted Gross Income)

No Money Management Fees

Incontestable and Private

Creditor Protection

Doesn't Have To Go Through Probate

No Contribution or Income Limits

Privacy, Flexibility and Control

Income does not Increase IRMAA (Income-Related Monthly Adjustment Amount)/Medicare premiums

The Ability to Earn Double Digit Returns

Tax-Free Death Benefit to Heirs (An immediate estate)

Three IRS Codes That Make It Possible – 101 (a), 72 (E) and 7702

The Answers are found in

Internal Revenue Code Sections and Tax Law:

101(a)

Tax-Free benefit

Tax Equity and Fiscal Responsibility Act of 1982. Minimum Amount of insurance required to qualify for the tax-free status.

Changed to The Deficit Reduction Act 1984

101 (a) is the tax-free death benefit. Where it blossoms over and above the account value, once any loans have been repaid, can be transferred to the beneficiary income tax-free.

72(e)

Tax-Free Growth

72(e) is tax-free accumulation

7702

Tax-Free Access

The Technical and Miscellaneous Revenue Act (TAMRA) of 1988. How fast you can put your money in

Section 7702, permanent life insurance is permitted to provide a source of income in retirement that is not counted as income or taxed as income because this income is considered a loan against the cash value of the policy.

3 Types of Retirement Accounts

Tax-Deferred

Employer Sponsored Accounts

You Don’t Own

1st is Money Manager

2nd is Broker Dealer

3rd is Wall Street

4th is IRS

5th is You

Is Always at Risk

1-3% Money Management Fees

Plus Huge Hidden Fees!

Adds Taxes (Triple Compounding)

Contribution Limits

Tax-Free

Individual Accounts

Self- Fund or Self-Direct

1st is You

2nd is Your Family and/or Business

Greater Control of Allocation

Greater Control of Income vs 4%

Greater Control of Living Benefits

Greater Control of Inheritance

Your Principal Balance is Always Protected

No Money Management Fees

Earn Stock Market Returns with ZERO RISK!

No Contribution Limits

Tax-Deferred

Brokerage Accounts

You Don’t Control

1st is Money Manager

2nd is Broker Dealer

3rd is Wall Street

4th is IRS

5th is You

Is Always at Risk

1-3% Money Management Fees

Plus Huge Hidden Fees!

Adds Taxes (Triple Compounding)

Contribution Limits

We are independent insurance producers that pride ourselves on providing innovative and creative strategies, with some of the largest, well-known, and reputable insurance companies in the industry. This website may contain concepts that have legal, accounting and tax implications. It is not intended to provide legal, accounting, tax or investments advice. By contacting us, we offer education and information regarding insurance strategies that may provide tax advantages along with index annuity options. © 2025